Introduction

Out of what is widely acknowledged as a blatant violation of international law, the entry of United States forces into Venezuela has produced one piece of good news for Guyana. Whatever the legal controversy surrounding that intervention, its practical effect has been to neutralise Venezuela’s capacity to pursue its fanciful claim to the entire Essequibo. We are unlikely to see Venezuela revive that claim for several decades, if ever. When the International Court of Justice eventually pronounces on the matter – presumably in Guyana’s favour – it will be confirming a geopolitical reality already established.

However, the US intervention has also brought with it economic uncertainty, reshaping the global economy, particularly in energy markets. While one existential threat has receded, another has quietly emerged – not from Caracas, but from Washington and the broader economic fallout of the Trump solution to the Maduro problem. Now the economic headwinds identified in Guyana’s Mid-Year Report have been forcefully strengthened. Oil prices are revised downward, global uncertainty is elevated, and key export commodities were acknowledged as facing “mixed price dynamics” presenting both risks and opportunities.

Before Venezuela, consensus projections already pointed to oil at around US$60 a barrel in 2026, reflecting weak demand and ample supply. Post-Venezuela, and with Donald Trump focused squarely on the 2026 midterm elections, the centre of gravity has shifted decisively toward US$50 oil as a political objective. Trump needs oil prices down to contain inflation and manage electoral risk, and markets have learned that when he signals a price preference, policy follows. Guyana will not be immune.

Not that the price outlook mean falling domestic output. Guyana’s production will continue to rise as additional FPSOs come on stream and in the short-term, higher volumes will partly offset the lower price per barrel. But with US oil majors now invited to follow Trump’s lead back into Venezuela, those same companies will have to balance production against sales across their global portfolios. In a crowded market, that balancing exercise can affect where and how limited investment dollars are allocated among competing destinations.

Time to take stock

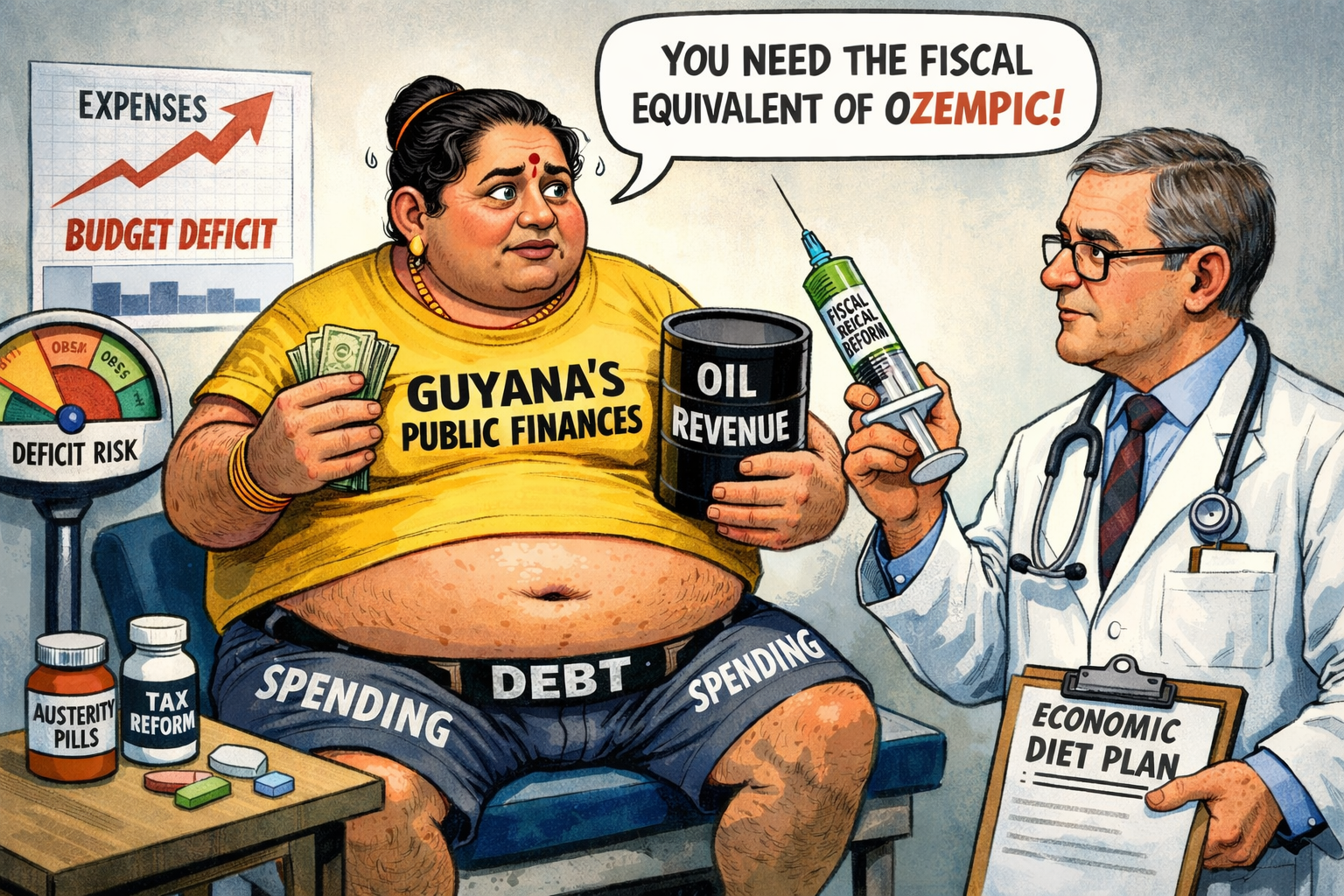

This choice and decision-making applies equally to us in Guyana where the oil sector towers over everything else and therefore demands attention at the highest levels. A US$50 oil environment is not a crisis scenario, but if not properly addressed can become one. Even as the MidYear Report acknowledges heightened global uncertainty and oil-price volatility, it also records, in boastful terms, accelerating expenditure, expanded commitments, and rising recurrent obligations. The implicit assumption is that today’s revenues will persist long enough to absorb tomorrow’s costs. History, including Guyana’s own, offers little support for that confidence.

Much of the spending now being normalised is structural rather than temporary: wages, transfers, subsidies, and large capital projects with high and continuing operating costs, and the new and growing discretionary funds with vague line descriptions. Once embedded, they reduce fiscal room and force governments to respond to shocks through borrowing, drawdowns, or abrupt retrenchment. As governments face criticisms from their constituents they spend more, not less, to appease them even if such spending is carried out without any regard for the law or concern for accounting and transparency.

Underlying this spending approach is a governing assumption that has hardened into doctrine. The PPP/C’s administrations and Ali’s in particular treat annual increases in the national budget as an occasion to crow, as development, and as an article of faith. Large, highly visible projects – Silica City and the Palmyra stadium foremost among them – are embraced as symbols of progress, alongside talk of another bridge in Berbice, another gasto-shore project, and yet another stadium. Each is presented largely in isolation, rarely within a coherent medium-term fiscal framework, and seldom accompanied by a serious accounting of opportunity cost or long-run burden. In an economic downturn, these projects become white elephants even as they carry maintenance costs.

What makes this posture especially troubling is, as noted above, the risks are not unrecognised. Indeed, the Mid-Year Report identified global uncertainty, oil-price volatility, and macroeconomic vulnerability. Coming from an accomplished public-finance specialist, that recognition carries weight. But recognition alone is not enough. It imposes a duty to act. That duty should now find expression in the budget process itself. The pending 2026 Budget presents a clear opportunity to introduce credible medium-term fiscal rules, expenditure ceilings, and disciplined sequencing of major projects. Any delay – whether for extradition or any other extraneous purpose would signal politics over policy. In an economy as exposed as Guyana’s now is, that choice constitutes a further risk.

A sustained fall in oil prices would also have wider consequences. Fewer oil dollars mean less foreign exchange entering the economy, increasing pressure on imports and the exchange rate. Combined with constrained spending, this raises the risk of inflation even as growth slows, while delayed projects and tighter cash flows increase the risk of job losses, particularly in construction and services.

Conclusion

Put bluntly, the Government needs to wean itself off its reliance on spending steroids. Years of aggressive fiscal stimulation may have produced attractive outcomes and headline growth, but they have also dulled discipline and restraint. Endless injections of expenditure are no substitute for planning, sequencing, or endurance. What Guyana’s public finances now require is the fiscal equivalent of Ozempic – a firm and sustained dose of appetite control to curb the compulsion to spend simply because there is no obvious restraint. Without that restraint, excess will continue to be sold as progress, until today’s choices harden into structural costs that are economically damaging and politically impossible to reverse.

Chris Ram