We’ve recently published the first article in a new series examining offshore gas development in emerging producer states.

Discovery is the easy part.

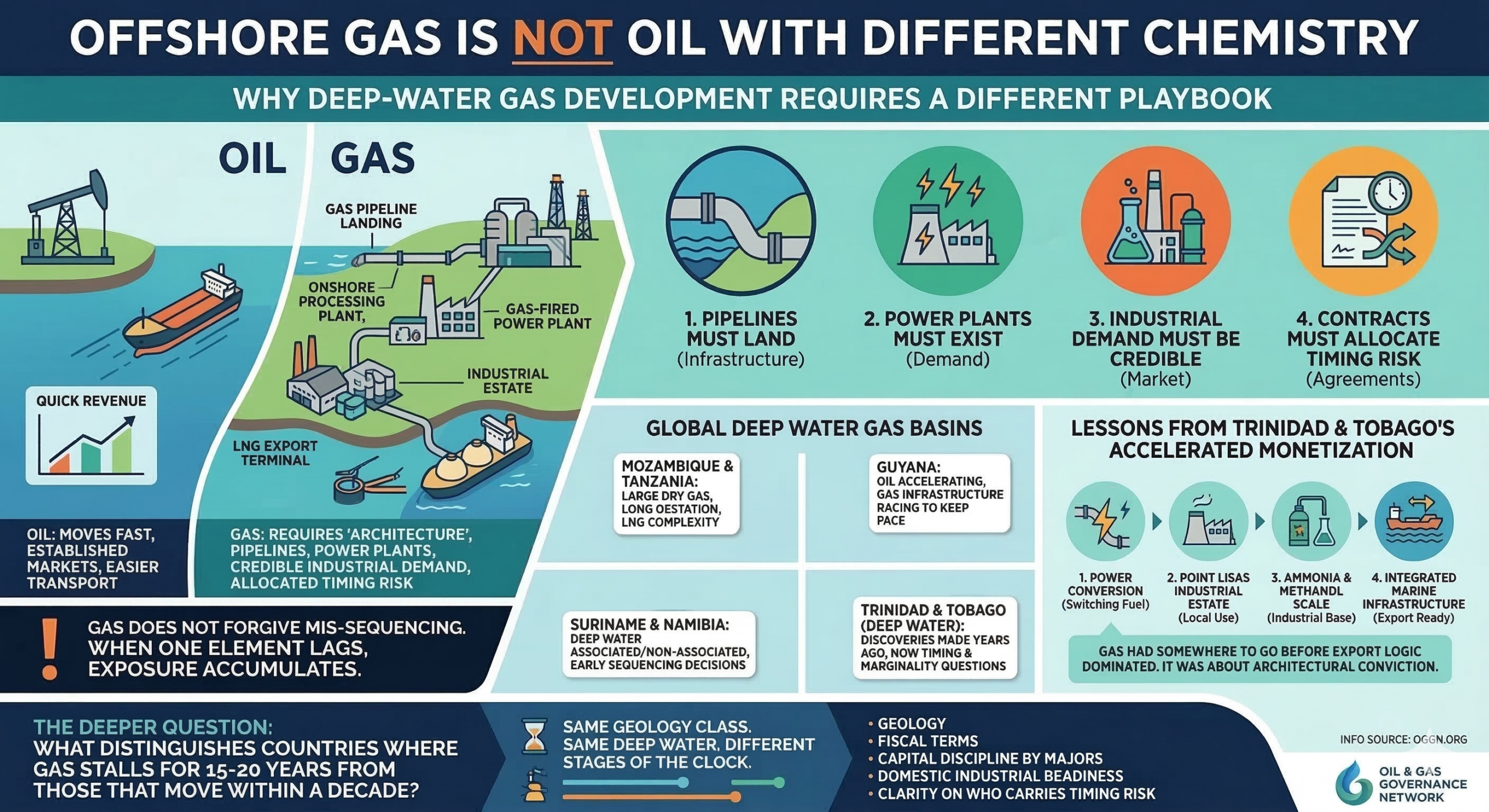

Development — especially in deep water, without ready markets — is where the real variables emerge.

Oil can move fast.

Gas requires architecture: Pipelines must land. Power plants must exist. Industrial demand must be credible. Contracts must allocate timing risk clearly.

When one element lags, exposure accumulates.

We’re seeing different versions of this across basins:

• Mozambique & Tanzania — large dry gas discoveries, long gestation, LNG complexity.

• Guyana — oil accelerating, gas infrastructure racing to keep pace.

• Suriname & Namibia — associated and non-associated gas in deep water, early sequencing decisions underway.

• Trinidad & Tobago (deep water) — discoveries made years ago now confronting timing and marginality questions.

Same geology class. Same deep water. Different stages of the clock.

In the coming articles, we’ll examine what each can learn from the others -particularly how contract design, market creation, infrastructure sequencing, institutional capacity and capital allocation choices shape outcomes.

Gas does not forgive mis-sequencing.

One of the upcoming pieces in this series will revisit a different Trinidad story.

Before LNG scale, before global spot markets — Trinidad deliberately accelerated gas monetisation by building domestic demand architecture:

• Power conversion • The Point Lisas industrial estate • Ammonia and methanol scale • Integrated marine infrastructure

Gas had somewhere to go before export logic dominated.

That sequencing mattered.

It wasn’t about perfect governance. It was about architectural conviction.

There are lessons there for new producers navigating oil-first momentum with gas trailing behind.

The deeper question I’ll explore:

What distinguishes countries where gas stalls for 15–20 years from those that move within a decade?

Is it geology? Fiscal terms? Capital discipline by majors? Domestic industrial readiness? Or clarity on who carries timing risk?

Each basin answers differently.