Income from new shallow-water blocks offshore Guyana versus Gulf of Mexico

Minister Vickram Bharrat was pleased to remind the National Assembly during the second day of the Budget 2026 debates that Guyana had gained USD 22 million from ‘two recently signed petroleum agreements’ (https://dpi.gov.gy/ppp-cs-transparent-oil-management-sets-guyana-apart-from-coalitions-secretive-record-min-bharrat/). It was not clear from where the Minister found his USD 22 million. The publicly accessible announcements are for (1) a signing bonus of USD 15 million on the PSA with a consortium of TotalEnergies (40% share and the operator), Qatar Energy (35%) and Petronas (25%) for shallow-water block S4 (178,800 ha; https://dpi.gov.gy/guyana-secures-us15m-signing-bonus-for-new-oil-agreement/ ) in November 2025 and (2) a signing bonus of USD 17 million on the PSA with Ghana’s Cybele Energy for shallow-water block S7 (200,000 ha; https://guyanachronicle.com/2025/12/09/guyana-gets-us17-million-in-signing-bonus-from-ghanas-cybele-energy-for-s7-block/) in December 2025. Minister Vickram Bharrat seems to have lost USD 10 million from the two signing bonuses (15+17-22=10), but no Member in the National Assembly seemed to be concerned.

Compared with the USD 18 million signature bonus for the Stabroek Tract in 2016, the recent signature bonuses for shallow-water blocks S4 and S7 are indeed an improvement, as shown in Table 1.

In contrast to Guyana’s inability to negotiate effectively with petroleum companies, the US Bureau of Ocean Energy Management (BOEM) leases mid-water blocks (400+ metres in depth) in the Gulf of Mexico through competitive bidding. In 2026, the typical 10-year leases for a standard concession of 3×3 square miles (2331 ha) attracted signature bonuses greater than USD 247 per hectare.

And the US oil leases in the Gulf of Mexico also pay annual rent and royalty to the US BOEM at much higher rates than do oil companies in Guyana’s offshore petroleum tracts or concessions, as shown in Table 2.

Compare income from the Marcellus Shale gas fields, Pennsylvania

If we look at the petroleum-based income of private landowners with lands above the Marcellus Shale oil and gas fields in Pennsylvania (USA), we can see an even greater difference from Guyana. Private landowners, depending on the land tenure type, may have property rights to the underground minerals, oil and gas. The gas fields are enormous and the rights are valuable. An individual lease to a gas extraction company is often 1 square mile (258 hectares) for 5 years, with 6-10 well pads spread across the square mile. Signature bonuses are around USD 5000/ha, nearly 60 times the bonuses paid to Guyana in 2025. Royalty on gross production is, by law in Pennsylvania, a minimum of 12.5%, but more usually 15-20%, compared with the 2% for the Stabroek PSA and 10% for the new Blocks S4 and S7 in Guyana. Rental payments on the 1-ha well pads and access roads may be as high as USD 100,000/ha. Total petroleum lease income is more usually around USD 75-100,000/ha over the 5-year leases.

Longtail gas-condensate more like Pennsylvania

Why is this relevant to Guyana? Because the Longtail field is a retrograde gas-condensate field with a production capacity of 1.2-1.5 billion standard cubic feet per day of non-associated gas (about 8 times the Liza-1 production of 180 million standard cubic feet per day of associated gas). ExxonMobil is looking to sell the gas leftover from reservoir re-injection, in addition to the 250-290,000 barrels/day of very light condensate; https://kaieteurnewsonline.com/2026/02/19/exxon-gears-up-for-eighth-project-seeks-year-end-govt-approval-routledge/. While the government is considering a second gas-to-energy project, with an ExxonMobil-constructed pipeline from the Longtail field to Berbice (https://kaieteurnewsonline.com/2025/02/20/exxonmobil-proposes-new-pipeline-to-transport-gas-to-berbice/ and https://kaieteurnewsonline.com/2026/02/18/govt-eyes-partnership-with-suriname-for-second-gas-project-in-berbice/), Exxon may also be looking to direct export of the gas from a FPSO fitted with gas cleaning/drying/compressing facilities, so different from those seven FPSOs now in service or under construction. The financial profile of the Longtail field with a projected life of 30 years also differs from the previous fields like Liza-1 and Payara.

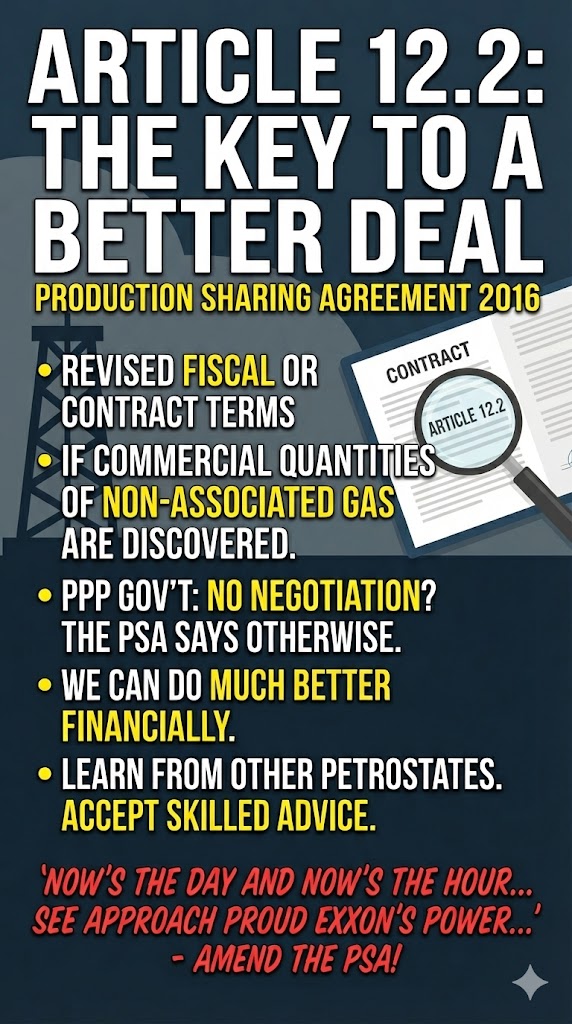

Revision of the PSA 2016

Article 12.2 of the Production Sharing Agreement 2016 provides for ‘revised fiscal or contract terms’ if commercial quantities of non-associated gas are discovered. Remember that the PPP governments have insisted that no negotiation of the PSA can be considered? The possibility is right there, in the PSA. We can do much better financially, with reference to what other petrostates have negotiated with the major oil companies, taking up the abundant skilled advice which was then offered and rejected in 2016. Amending the words of William Wallace’s Scottish battle song, ‘Now’s the day and now’s the hour / See the front of battle low’r / See approach proud Exxon’s power / Chains and slavery’.